Diesel transport was once the standard. That era has passed.

The year 2040 runs on clean and efficient systems.

Zero-emission vehicles—powered by renewables—enable trade and deliver access to markets and mobility for people without compromising the health of the communities they serve. Corridors lined with fast chargers connect ports, cities, rural communities and nations across borders. With technology integration, energy storage, and vehicle-to-grid capabilities, fleets stabilize the distribution network, adding resilience and helping balance loads. Stable grids and continuous power are the norm.

The logistics sector is reshaped—goods are transported more efficiently, digital systems seamlessly integrate across borders.

Cities thrive with green spaces where zero-emission zones and reclaimed streets put people at the center of urban planning. Children play outdoors breathing healthy air. Communities are connected and inclusive, powered by microgrids and infrastructure that enhance quality of life for all. And in a remarkable shift emerging market countries have leapfrogged diesel and established themselves as leaders in advanced systems like vehicle technology and infrastructure design.

These are the tangible outcomes of the Global Memorandum of Understanding on Zero-Emission Medium- and Heavy-Duty Vehicles (Global MOU)—and its ambition to reach 100% new zero-emission medium- and heavy-duty vehicle (ZE-MHDV) sales by 2040—delivered worldwide.

The journey to Destination 2040 continues here in the new digital edition of the Multi-Country Action Plan 2025. Inside, you’ll find fresh insights on global zero-emission medium- and heavy-duty vehicle trends, inspiring deployments, and bold actions from endorsers and signatory countries. You’ll also see what’s needed to fully unlock this transition—driving cost savings for businesses, creating careers in the green economy, and securing clean air and better health for every community.

Bumps in the road

While growth of ZE-MHDVs remains steady, three bumps in the road impede accelerated and widespread adoption.

Market Uncertainty

Markets need certainty to transform. Fragmented policies, a lack of regulation and uneven incentives make it unnecessarily difficult for stakeholders across the commercial vehicle sector to plan, invest, and scale. Outdated vehicle standards, unpredictable energy prices and a lack of support for fleets are part of the landscape. Few will argue against the value of market certainty that regulation creates.

Incomplete Infrastructure

The lack of sufficient charging infrastructure, especially for long-haul operations and remote areas, remains one of the biggest barriers to ZE-MHDV adoption. This challenge is compounded by limited grid capacity in many regions, which cannot yet support the fast-charging needs of fleets at scale.

Inaccessible Financing

Cost remains a major hurdle. While ZE-MHDVs offer clear long-term savings in fuel and maintenance, their high upfront purchase price continues to deter adoption, particularly compared to diesel trucks. Financing barriers, including the cost of capital and insurance, add further complexity for fleets looking to adopt cleaner technologies.

On the road to Destination 2040, there is no time to lose. The barriers ahead are real but far from insurmountable. Proven solutions already exist to overcome these challenges and accelerate progress. As policies take shape and costs continue to fall, businesses have a central role to play through investment, innovation, and collaboration across sectors and borders. With total cost of ownership (TCO) already reaching parity for some vehicle segments and nearing parity for others, building a strong business case ahead of schedule will be essential to meeting global climate goals, lowering costs for consumers, and creating a more resilient transportation system that protects the communities it serves. To understand the path forward, we must first take stock of where we stand today and how emerging solutions can bring us closer to realizing Destination 2040.

Powering the Shift

Zero-emission vehicles are redefining what’s possible, delivering benefits that even the most advanced diesel trucks cannot match. Already serving fleets of all sizes, they are achieving cost parity faster than anticipated and giving operators a competitive advantage in moving goods more efficiently and at lower cost.

“We’re not just decarbonizing—we’re rewiring the global economy. What makes this moment so powerful is that stakeholders—utilities, OEMs, governments, and local communities—aren’t just aligned in purpose; they’re discovering shared value. The transition to ZE-MHDVs isn’t a zero-sum game—it’s a multiplier, generating cleaner air, better jobs, and new economic engines where they’re needed most.”

Stephanie Kodish – CALSTART/Drive to Zero – Global Senior Director

Yet, emissions from the transportation sector continue to rise, underscoring the urgency of deploying solutions that address both immediate and long-term needs. As OEMs expand production and introduce more diverse models, falling battery prices are driving down upfront costs across most markets, making adoption increasingly attainable.

While policy progress in the United States remains uncertain, momentum is accelerating across the European Union, China, and emerging economies that are positioning themselves as hubs for clean technology and innovation. Meanwhile, large shippers and carriers are demonstrating what is possible through large-scale zero-emission truck deployments, using aggregated procurement and creative leasing models to strengthen their competitiveness and speed the transition.

The Global MOU on Zero-Emission Medium- and Heavy-Duty Vehicles

In 2021, the Global Memorandum of Understanding (Global MOU) on Zero-Emission Medium- and Heavy-Duty Vehicles (ZE-MHDVs) was launched at the United Nations Climate Change Conference (COP26) in Glasgow, Scotland. The landmark agreement calls for signatories to achieve 30 percent new sales of ZE-MHDVs by 2030 and 100 percent new sales by 2040. With 15 governments forming the initial cohort in 2021, it marked a major step forward in elevating the ambitions for global MHDV decarbonization. This year the Global MOU welcomed the addition of Mexico, Montenegro, and Peru as signatories, continuing to elevate ambition and grow momentum across the world.

National Government Signatories to the Global MOU on Zero-Emission Medium- and Heavy-Duty Vehicles as of 2025

Today, the number of country signatories has grown to 41 strong, with more than 280 endorsers and knowledge partners encompassing the private sector, non-governmental organizations (NGOs), and sub-national governments. With growth in sales, continued development of policy and regulatory frameworks by governments, and deeper engagement by the private sector to establish profitability and scalable business cases for the technology, the time for action is now.

Global progress towards ZE-MHDVs

It is now more important than ever to focus collective efforts to achieve the ambitions set forth in the Global MOU to enable healthy communities, clean air, and thriving business—and decouple the movement of goods and people from the emissions contributing to climate change and harming public health.

Emissions

Transportation is one of the largest contributors to global climate pollution, responsible for about 21 percent of global carbon dioxide (CO₂) emissions and more than one-third of emissions from consumers. Road vehicles, including cars, trucks, and buses, produce nearly three-quarters of all transport-related CO₂. Among them, diesel trucks and buses are both a rapidly growing climate threat and a major source of harmful air pollution. Between 2020 and 2050, freight-related greenhouse gas emissions are expected to double, while fine particulate matter (PM2.5) from diesel combustion could rise by more than 40 percent, threatening the climate and public health worldwide.

“This is the second sector with most emissions in the country but, as well, it represents a change in the social aspect. So, it will mean as well not only the reduction of emissions, but also a transformative way for people to access to different connection points through transportation.”

Pamela Abreau – Cambio Climático – Dominican Republic – Head of Mitigation Department

Diesel vehicles generate 73 percent of on-road nitrogen oxides (NOₓ) and 60 percent of particulate matter, causing over 330,000 premature deaths annually and more than $1 trillion in yearly health damages. The impacts fall disproportionately on communities near highways, ports, and industrial centers where emissions are concentrated.

Although they make up only 4 percent of vehicles worldwide, trucks and buses consume 36 percent of on-road fuel and emit a similar share of greenhouse gases.

Impact of HDVs on Global Fuel Consumption and NOx Emissions

Destination 2040 promises a cleaner and more sustainable future for all, and by meeting the goals of the Global MOU could prevent 7.8 gigatons of CO₂ emissions between 2025 and 2050, equal to 877 billion gallons of gasoline burned. Rapid, coordinated decarbonization of medium- and heavy-duty vehicles is essential to achieving global net-zero goals and meeting the commitments of the Paris Agreement.

Vehicle sales and deployment trends

The Largest Fleet Retrofit Project in the World

Learn how Zeronox and the Jospong Group have partnered to execute the world’s largest fleet retrofit electrification project, transforming 1,000 internal combustion engine (ICE) refuse trucks in Ghana into zero-emission vehicles using the proprietary Electric Powertrain Platform (ZEPP). With an initial pilot phase complete, the project is now entering mass deployment.

Battery-electric vehicles may seem like a modern breakthrough, but their roots stretch further back than the combustion engine itself. The earliest cars relied on cumbersome lead-acid batteries, and despite their promise, they fell short with limited charging infrastructure and shorter ranges. Now, a century and a half later, electric propulsion has returned—not as a novelty, but as the defining force of a new transportation era. In fact, battery-electric vehicles are about 65% more energy efficient than combustion engines, converting 80–90% of electricity into motion compared with just 15–25% for gasoline. Even when accounting for battery production, they produce roughly 63% fewer lifecycle emissions.

Battery prices fall

Today, batteries are reaching cost milestones that fundamentally reshape the economics of zero-emission transport. From 2023 to 2024, battery pack prices fell 20%, largely due to manufacturing capacity expanding faster than global demand. Critically, EV batteries have now dipped below $100/kWh, a threshold pivotal for market competitiveness. Regional variations remain, but advances in chemistry, manufacturing, and materials, together with increased global competition, are set to drive costs for ZE-MHDVs even lower.

Lessons from light-duty EVs

Today, electric cars are well on their way to dominating the passenger vehicle market, with prices falling, more options coming to market, and significant cost savings to be realized. Already in 2024, Norway has achieved over 95% new sales of electric cars. China has reached about 50% of total sales being electric. While trends in the U.S. suggest a slowdown, sales are still up year-over-year in 2025. Other geographies show no sign of slowing down. Similar trends are emerging in the Global South. Countries like Vietnam, Brazil, Mexico and Thailand are also enjoying rapid growth in the EV passenger car segment largely driven by affordable models coming from China. These trends speak to the rapidly advancing state of technology and comfort that consumers have found and give a positive outlook to what is to come in the medium and heavy-duty sector.

Buses

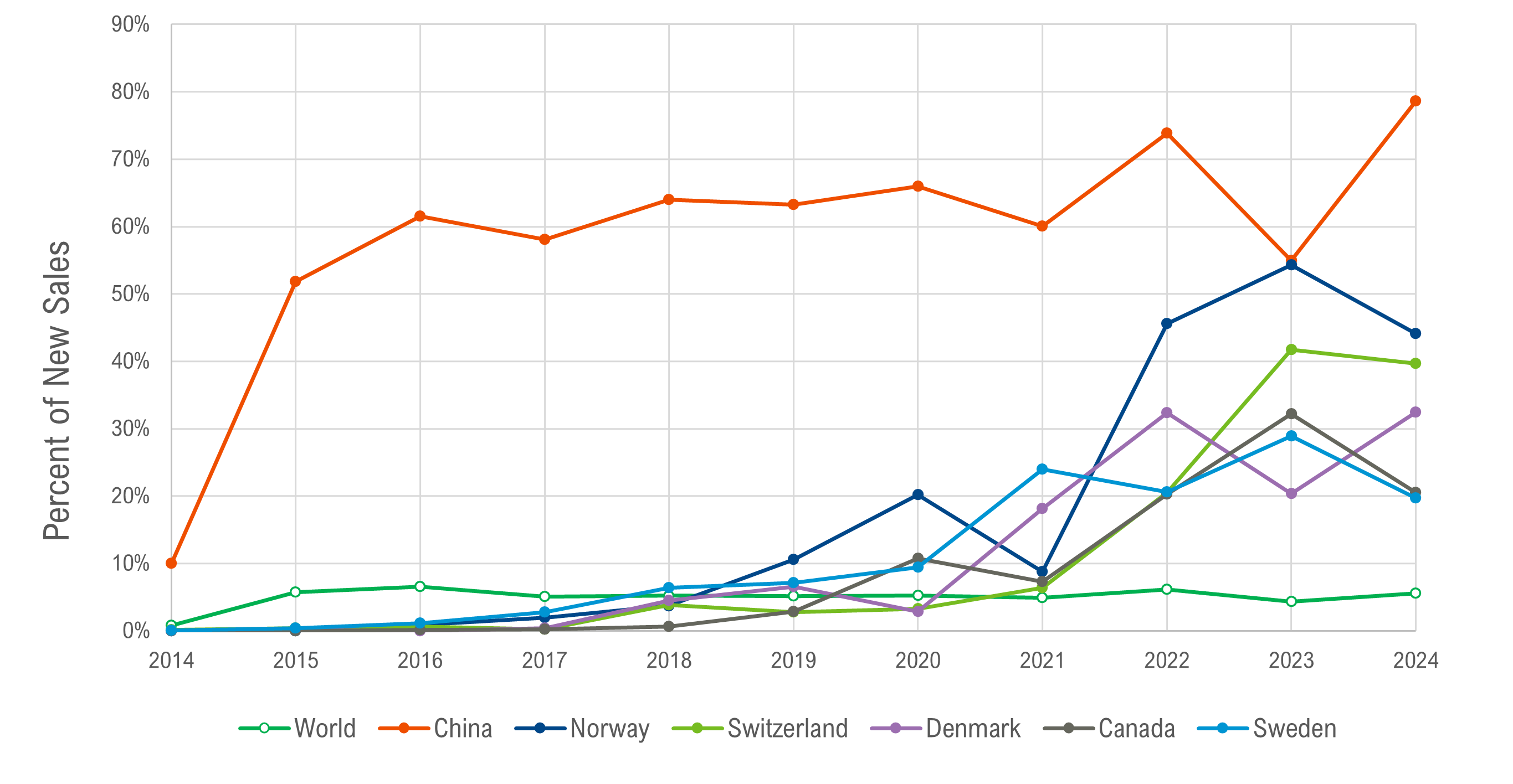

Globally, zero-emission buses (ZEBs) have achieved a sales share of approximately 5.5% of all buses sold as of year-end 2024, equating to about 68,000 units and remain a key segment for electrification across markets. Typically running along well-established routes that frequently return to the same domicile on a daily basis, ZEBs are positioned well for rapid scaling up in cities across the world. Notable examples include Shenzhen, which pioneered one of the world’s first fully electric city bus fleets. These achievements extend well beyond China. In Santiago de Chile, innovative approaches to bus tendering, financing, and contracting have transformed the city’s public transport system, resulting in the second-largest electric bus fleet outside of China. In Bogotá, Colombia, one of the Global MOU co-leads, electric buses already represent over 40% of the fleet and continue to expand rapidly. Likewise, Denmark, Belgium, Norway, and Switzerland have reached electric bus sales shares of around 40%, underscoring the growing global momentum toward zero-emission public transport.

Annual sales share of new zero-emission buses by global leaders

Truck sales growth

From Diesel to Decarbonization: A New Era for Chilean Logistics

This groundbreaking project delivered Chile’s first fleet of electric heavy-duty trucks for Walmart Chile—ushering in a new era of clean, quiet, and efficient freight. Today, more than 50 electric trucks power deliveries across Santiago proving that zero-emission freight can move goods at scale while slashing emissions and noise pollution—bringing cleaner air and quieter streets to the communities along its routes.

Since a brief slowdown in 2021, sales of zero-emission trucks have been making steady gains year over year. In 2024 approximately 107,800 units were sold in markets across the world, accounting for approximately 2% of all truck sales. Of these sales, about 81,000 were heavy-duty trucks, representing a doubling year-over year. While the sales concentrated in China, with an annual ZET sales share of 4.8%, noteworthy gains were observed in several European countries as well. In Switzerland, Norway, Denmark, and Sweden, where winter temperatures routinely drop below freezing, sales shares topped 7%. These results don’t just challenge old assumptions—they dismantle them, proving that zero-emission trucks can deliver in any climate.

Further, when considering specific vehicle types such as medium-duty trucks, the progress goes parabolic, with countries like the Netherlands, Denmark, and Sweden all clocking in at above 50% ZE-MDT sales in the first half of 2025.

Annual sales share of new zero-emission trucks by global leaders

Zero-Emission Truck and Bus Model Availability

As of the end of 2024, ZE-MHDVs, including buses, have reached a global market share of approximately 2.6 percent, a near doubling from 5 years ago when the Global MOU was launched. While China accounts for most of these sales, other countries with supportive policies are rapidly narrowing the gap.

According to Drive to Zero’s Zero-Emission Technology Inventory (ZETI), as of this 2025 assessment there are 974 ZE-MHDV models available worldwide across 10 vehicle categories. The figure below illustrates this growing diversity, showing model availability by vehicle type (trucks, buses, and vans) and by major geographic region.

While model availability is a key indicator of market progress, ZETI also uses detailed vehicle specifications to reveal insights and trends that help track the rapid evolution of the zero-emission vehicle market. The figures above, sourced from the ZETI Data Explorer, allow users to explore which models are available, where they are offered, and how the market is developing.

Growth of ZE-MHDV models across regions in 2025 (left) and ZE-MHDV models available by region and vehicle category in 2025 (right)

Zero-Emission Technology Inventory (ZETI) – Is an interactive online database tracking commercially available zero-emission medium- and heavy-duty vehicles (ZE-MHDVs) worldwide. It provides fleets and policymakers with detailed specifications, regional availability, and production timelines. The complementary ZETI Data Explorer builds on this database, allowing users to visualize, compare, and filter global market trends by vehicle type, region, and technology—offering a comprehensive view of the evolving zero-emission vehicle landscape. ZETI ToolZETI Data Explorer

Adoption by large global shippers and other success stories

Partnership is Leadership: Electrifying U.K. Freight

The Zero Emission HGV & Infrastructure Demonstrator (ZEHID) Programme, launched in October 2023, is a UK government initiative backed by £200 million to accelerate the adoption of near-zero emission trucks. As part of this partnership, DFDS secured funding for eight electric HGVs and depot charging infrastructure, supporting its commitment to achieving net zero emissions by 2050.

Multinational fleets and major shippers play a pivotal role in accelerating the transition to clean transportation. Their ability to harness detailed operational data, realize substantial fuel savings, and aggregate demand positions them to move the market. Already, companies such as Amazon, Maersk, and DHL are proving that demand for zero-emission technology is strong today. In addition to the largest fleets, there must also be steady action from smaller fleets, supported by programs that reduce costs, bridge knowledge gaps, and accelerate charging infrastructure.

Amazon

By 2024, Amazon deployed more than 25,000 custom Rivian electric vans in the U.S. and 5,000 across Europe. The company has also integrated 50 heavy-duty electric trucks into its Southern California operations and placed orders for 200 more in the UK and Germany. Supporting this fleet, Amazon has installed over 32,000 chargers—enabling more than 1 billion packages to be delivered in zero-emission vehicles in 2024 alone.

Maersk

As both a logistics powerhouse and a Global MOU endorser, Maersk is accelerating the transition to zero-emission freight. Already operating over 300 heavy-duty electric trucks in North America and Europe, Maersk is extending its reach into emerging markets such as Chile, partnering with Sotraser to pioneer electrified port drayage operations.

DHL

As a major global logistics provider and leader in last-mile delivery, DHL is rapidly expanding its zero-emission fleet. With several hundred heavy-duty electric trucks and more than 30,000 electric vans deployed in North America and Europe, the company is demonstrating that large-scale electrification of freight and delivery is both practical and underway.

Ultratech Cement – India

Global progress continues with India’s Ultratech Cement, the nation’s largest cement company, taking bold steps to electrify heavy-duty freight. The company has contracted 100 electric trucks, with 5 already in operation, and is targeting 500 by year’s end. Transporting nearly 75,000 metric tonnes of raw material each month, the fully deployed fleet is expected to deliver significant climate benefits, reducing an estimated 17,000 metric tonnes of CO₂ annually, all while setting an industry precedent.

Country and regional policy leadership

Policy remains a cornerstone of the ZE-MHDV ecosystem. While business leadership has demonstrated the viability and momentum of zero-emission technologies, enabling widespread adoption requires supportive and sustained policy frameworks. The following examples highlight countries and regions advancing ambitious approaches—many aligned with the Global MOU targets for ZE-MHDV adoption—to accelerate deployment. These were selected for their potential to influence global market dynamics, their leadership in regulatory approaches, and their ability to drive systemic change—despite varying levels of federal alignment, as seen in the United States. Together, they illustrate the critical role of policy in providing market certainty and a level playing field for OEMs, investors, and infrastructure providers Strong regulation can accelerate progress and help build on the successes achieved to date.

E.U.

As of 2025 Europe has established the world’s most ambitious regulatory framework for zero-emission medium- and heavy-duty vehicles. Binding EU CO₂ standards require truck makers to cut emissions 45% by 2030, 65% by 2035, and 90% by 2040, while city buses must transition to 100% zero-emission sales by 2035.

The Alternative Fuels Infrastructure Regulation (AFIR) mandates truck-capable charging and refueling networks along major corridors, ensuring infrastructure keeps pace with vehicles. Third, beginning in 2027, a major revision to Europe’s Emissions Trading System (ETS 2) will add a carbon price to transportation fuels, raising diesel costs and making combustion engine vehicles more expensive to operate. In parallel, many European cities are rolling out zero-emission zones and procurement mandates, creating powerful demand signals. This integrated “sticks and enablers” package provides manufacturers, fleets, and investors strong long-term certainty.

United States

The United States Environmental Protection Agency’s (U.S. EPA) Phase 3 GHG standards (covering model years 2027–2032) sets progressively tighter CO₂ limits for trucks. However, the policy environment is unsettled as the Trump administration is actively seeking to roll back these rules and the legal foundation for regulating greenhouse gases, creating major uncertainty and backtracking years of progress.

The state of California, a longtime leader in U.S. environmental policy, has also seen setbacks in two of the key pieces of regulation driving adoption. After congressional review in May 2025 California’s waiver under the Clean Air Act was withdrawn, stripping away the state’s ability to enforce the Advanced Clean Truck Regulation, a first-of-its-kind measure requiring truck OEMs to steadily increase their sales shares of zero-emission vehicles year-over-year. Even so, California remains committed to its goals of clean air and has brought a legal battle to the U.S. federal government asserting overreach of authority by the current administration.

These challenges in the U.S. market risk setting the country back against faster-moving parts of the world like China and Europe. Although investments in charging infrastructure and vehicle deployments continue, without strong federal support and with limits on states’ authority to regulate, the U.S. risks falling behind as other regions seize this pivotal moment to innovate, scale capacity, and expand market share. Left unchecked, this could ultimately drive higher costs for U.S. consumers and businesses.

China

In China, policy has been the driving force behind rapid zero-emission market growth. Much of the government’s focus has centered on subsidy schemes and ambitious industrial strategies designed to position the country ahead of the curve in manufacturing, critical material supply chains, and technical expertise. These policies have created market certainty for domestic and international investors while nurturing the talent and industrial capacity needed for consistent growth. Through sustained, large-scale investment in batteries and other zero-emission technologies, China has established itself as the global leader in medium- and heavy-duty vehicle decarbonization by sales volume and now produces more than 75% of the world’s batteries. Complementing these industrial policies are regulatory measures to lock in fuel efficiency improvements and ensure long-term competitiveness.

China’s update from Phase 3 to Phase 4 fuel consumption standards, which took effect in July 2025 will increase stringency by 12–16%, depending on vehicle category, with a two-year phase-in period before full enforcement in 2027. Together, these overlapping policies combine market driving mechanisms with regulatory certainty, enabling China to secure and double down on its leadership position in the global transition to zero-emission MHDVs.

India

Charging up Change: India

See how leader Ultratech is jumping on the opportunity for decarbonization with their deployments of heavy-duty zero-emission cement trucks in their industrial operations, meeting business and sustainability goals together

India is advancing a comprehensive policy framework to accelerate the adoption of zero-emission medium- and heavy-duty vehicles (ZE-MHDVs). On the supply side, the Bureau of Energy Efficiency (BEE) has proposed Draft Future Fuel Efficiency Norms (2027–2032) covering trucks (3.5–55t GVW), buses, and for the first time, light commercial vehicles. On the demand side, the Government of India has unlocked more than USD 3.2 billion through schemes such as PM Electric Drive Revolution in Innovative Vehicle Enhancement (PM E-DRIVE), PM e-Bus Sewa, and the PM e-Bus Sewa – Payment Security Mechanism (PSM). Together, these mechanisms will support deployment of over 30,000 ZE-MHDVs, including 19,671 vehicles under PM-EDRIVE alone.

At the sub-national level, Maharashtra has pioneered dedicated incentives for electric trucks and buses, complementing national initiatives. This layered approach combining central funding, regulatory tightening, and state-level action — highlights India’s ability to mobilize both capital and political will to advance ZE-MHDV adoption.

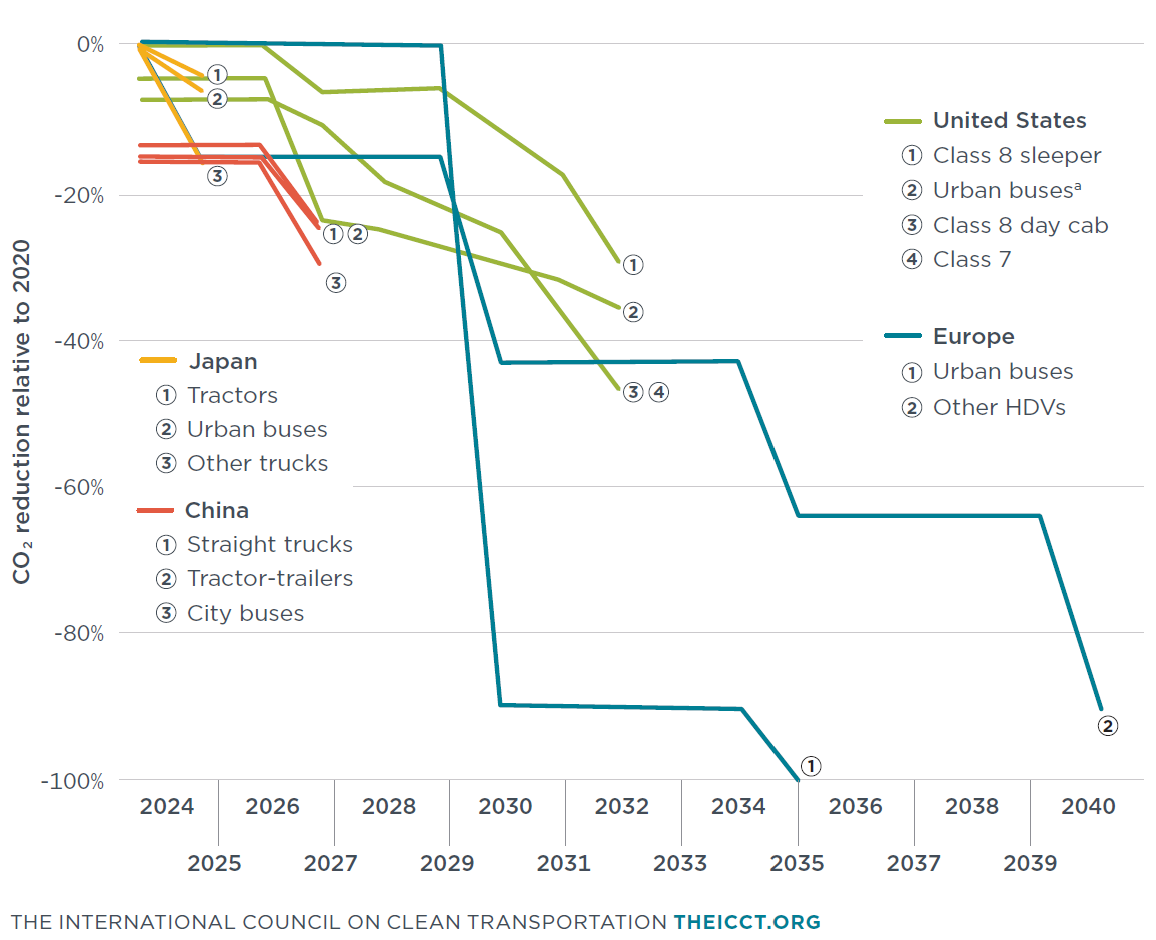

Comparison of improvements required for heavy-duty trucks from 2024 to 2040, relative to 2020 standard or baseline

Building the business case: The role of innovative finance

“This is a market with razor-thin margins, and once the cost parity is reached with diesel and electric vehicles or zero-emission vehicles are cheaper to operate over their lifetime, this transition is going to go so fast that in a blink of an eye the world will have changed.”

Sita Holtslag – CALSTART/Drive to Zero – Europe Director

Even though upfront costs for zero-emission trucks and buses remain high, total cost of ownership (TCO) is reaching cost parity in more and more real-world applications. In segments with high utilization and predictable routes, such as port drayage, last-mile delivery, and heavy-duty urban freight, fleets are already seeing lower operating costs compared to diesel. These use cases pair intensive daily operation with shorter ranges and access to reliable charging, allowing operators to maximize fuel and maintenance savings while minimizing downtime. Where vehicle prices are falling and energy costs are stable, ZEVs are not just environmentally sound, they are the best choice from a business perspective.

Access to affordable finance is key for fleets of all sizes to be able to make decisions based on total cost of ownership and not upfront costs. To enable fleets to act on favorable TCO, capital must be structured to reflect how these vehicles are used and where savings are realized. Emerging solutions such as residual value guarantees, as-a-service models, and utilization-linked finance are helping operators reduce exposure to uncertain resale values and variable duty cycles. At the same time, these mechanisms are expanding access for small and medium enterprises that often lack the balance sheets or borrowing histories to secure traditional loans. Together, these interventions are reframing zero-emission transport from a risk-associated purchase into an investable and advantageous asset class.

Still, as in any new market, risk perception remains high. Limited performance data, evolving policy signals, and unfamiliar asset classes lead to conservative lending and higher financing costs. The challenge ahead lies in demonstrating reliability, and building investor confidence so that zero-emission vehicles become the new normal as sound long-term investments.

Total cost of ownership

Assessing the total cost of ownership (TCO) offers a clearer picture of the business case for zero-emission medium- and heavy-duty vehicles (ZE-MHDVs). While their purchase price in some markets is still two to three times higher than diesel, long-term savings from cheaper electricity and lower maintenance can offset this premium. The balance hinges on three levers: bringing down vehicle costs, ensuring access to low-cost electricity, and maximizing vehicle and infrastructure utilization. Where these conditions align, ZE-MHDVs become cost-competitive more quickly. High-mileage operations in regions with low electricity rates will reach cost parity first, signaling where adoption may accelerate.

Median year of TCO parity between ZEV and ICE HDV in current literature by market and vehicle segment

This section outlines established and emerging mechanisms to manage costs and strengthen the business case for zero-emission operations. Beyond subsidies and risk management, fleets must take practical steps to optimize performance by right-sizing batteries, maximizing vehicle utilization, and using smart telematics and route planning to enhance efficiency. Where optimization alone is insufficient to make the economics work, targeted, temporary interventions by governments and development banks can help move a project toward bankability, supporting first movers who are willing to take on early risks.

Utilization-linked finance

“One of our key lessons in accelerating ZE-MHDV deployment is that operational efficiency, optimizing vehicle and driver utilization, whilst continuing to match business requirements, remains to be the main key to success. Developing the right business expertise and data-driven tools for intelligent route planning and charging management provide an integrated approach, ensuring that electric trucks are seamlessly integrated into existing logistics operations. Ultimately, successful ZE-HDV adoption hinges on optimizing every aspect of their deployment to meet existing business demands at competitive costs.”

Otto Gussenhoven – JUNA/Sennder – Head of Commercial Green Business & eMobility

Utilization risk, defined as the actual versus potential energy delivered at a charging site, poses a significant barrier to public charging infrastructure financing. Low or unpredictable utilization rates can deter investors and lenders from putting capital into a project, if it is not clear that the investee will generate sufficient returns to meet its financial obligations. To mitigate this, the commercial vehicle charging sector is adopting innovative business models. Shared charging sites (with access reserved to partner fleets) offer a similar certainty to depot charging by having secured users, while at the same time maximizing charging utilization by serving multiple fleets with complementary duty cycles. A variation of this is semi-public charging sites, where a fleet or fleets provide a baseload utilization, while opening chargers to third parties, at a cost, while not in use. This can allow fleets that are unable to install their own chargers to gain access, while creating an additional revenue stream for the fleets investing in infrastructure.

To further address early-stage utilization challenges, green banks and states have a crucial role to play. Flexible financing mechanisms, such as utilization-linked loans, provide temporary relief during periods of low utilization. Programs like the Canada Infrastructure Bank’s Charging and Hydrogen Refueling Initiative set a precedent for tailoring loan repayment terms to utilization rates: when utilization is low, borrowers pay less. As utilization grows and sites become more profitable, repayments also grow. These structures offer an alternative to subsidies that can still be effective at incentivizing early deployment and ensuring financial stability. Similarly, capacity credits embedded in programs like California’s Low Carbon Fuel Standard (LCFS) guarantee revenues for charging sites during critical ramp-up periods.

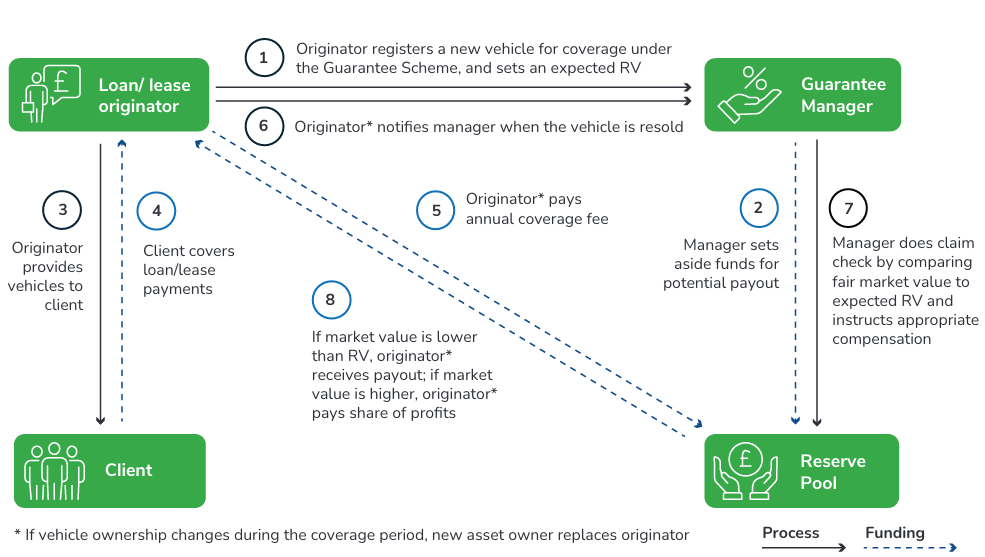

Residual value guarantees

Residual value (RV) is the expected future worth of a vehicle after a period of use, typically at the end of a finance or lease contract term. RV is traditionally based on historical vehicle resale data, which does not yet exist for ZE-MHDVs. Because of this, financiers tend to assign conservative (low) RVs when developing the financial terms for a truck loan or lease, in order to protect themselves from potential losses.

Financing payments are largely based on the difference between the delivery price of the vehicle and its residual value. As illustrated in the figure below, drawn from the Residual Value Guarantee Blueprint, a lower RV translates into higher periodic payments, and a higher RV into more affordable periodic payments.

Low RV results in higher periodic payments for fleet

Residual value guarantees (RVGs) are a proposed solution to mitigate potential losses for financiers if actual resale values end up being lower than the estimated RVs. By doing so, RVGs can encourage higher RV setting, and thus more affordable financing products. RVGs have gained support from cross-industry stakeholders as a promising mechanism to scale up investments in BETs. By mitigating RV risk, a RVG can reduce lease costs and increase access to finance, stimulating early demand and accelerating market maturity by 5–8 years. The following figure illustrates the technical set up of an RVG, but for a deep dive into the topic see the whitepaper linked here.

Commonly used structure from insurance and guarantee products across global markets

Credit risk guarantees

A common roadblock that fleets face when considering purchasing a zero-emission truck is finding favorable loan conditions. The majority of fleets on the road are small- and medium-sized operators—approximately 84% own between 1-6 vehicles. With very tight margins, many fleets struggle with creditworthiness and finding lenders who will offer favorable loans. Credit risk guarantees offer a tested approach to derisk this aspect of the financial value chain and help democratize access to ZE-MHDVs.

In California, this kind of mechanism has been deployed as a pilot to ease friction for SMEs looking to acquire ZETs. The California Zero-Emission Truck Loan Pilot builds on the success of the state’s legacy Truck Loan Program, providing financial continuity and stability for small fleets and lenders. Administered by the California Pollution Control Financing Authority (CPCFA) in partnership with the California Air Resources Board (CARB), the California Energy Commission (CEC), and major utilities such as Southern California Edison, the program launched a $30 million loan guarantee fund to expand access to capital for small trucking businesses. Using a loan-loss reserve system, the pilot supports qualified fleets of 20 or fewer vehicles purchasing new or used Class 2b–8 zero-emission trucks. For each eligible loan, CARB contributes 25 percent of the loan amount to a participating lender’s reserve account, which can be used to reimburse lenders in the event of a default, reducing financial risk and encouraging lending.

This de-risking mechanism enables lenders to extend credit on more favorable terms, making it easier for small operators with limited balance sheets to invest in zero-emission vehicles, charging infrastructure, and related equipment. The program’s flexible coverage and risk-sharing model help catalyze market entry, increase lender participation, and accelerate the adoption of zero-emission trucks across California.

Road tolls

Road tolls are an effective mechanism to accelerate cost-parity between zero-emission and combustion trucks. Two main types of tolls exist: distance-based and time-based. While both have been used in Europe, EU policy now requires Member States to adopt distance-based, CO₂-differentiated tolls for heavy vehicles to maximize climate and efficiency benefits. In practice, these tolls apply a charge per kilometer driven, adjusted for the vehicle’s size and emissions profile. Zero-emission trucks pay the lowest rates, often 50% or more below diesel trucks, while higher-emitting vehicles pay more. For example, Germany and Austria fully exempt zero-emission trucks from tolls today, while Denmark and the Netherlands are rolling out CO₂-based systems that will grant significant discounts to clean vehicles.

Low Carbon Fuel Standards

Low Carbon Fuel Standards are an effective and proven policy solution that leverages market-based mechanisms to incentivize the reduction of carbon intensity in transportation fuels. LCFS establish benchmarks for reductions in carbon intensity that ramp up each year. Suppliers that provide fuel below the benchmark generate credits, while those above must purchase them. In simple terms, this creates an economic incentive to install zero-emission charging infrastructure and dispense electricity and hydrogen to consumers as this will generate credits. In North America, along the west coast states of California, Washington and Oregon, as will as the Canadian province of British Columbia, LCFS programs have found great success in driving faster buildout of charging and refueling sites.

Putting innovative finance models to work in India

India’s investment landscape for ZE-MHDVs is rapidly developing to address key roadblocks, combining public funds, multilateral capital, and private finance to build a robust business case and speed deployments. The PM e-Bus Sewa–PSM scheme, with an allocation of ₹3,435 crore (~USD 410M), aims to mitigate payment risks and improve bankability of concession agreements. It will enable deployment of 38,000 e-buses by FY 2029, supporting operations for up to 12 years. This positions India for the world’s largest bus electrification push. Multilateral institutions are also stepping up: the IFC–World Bank Group has committed USD 157M to Indian OEMs and operators, enabling 4,000 e-buses and charging hubs across 39 municipalities while creating 12,000 jobs, many for women. Importantly, USD 57M went to two Global MoU endorsers — Transvolt Mobility (USD 20M) and GreenCell Mobility (USD 37M). Transvolt further became one of the first electric fleet operators from India and globally to issue a Sustainable Green Bond, raising funds to deploy 300+ heavy commercial EVs. These innovations illustrate how India is pioneering blended models of concessional, commercial, and sustainable finance — creating replicable pathways for the Global South while showing that ZE-MHDV investments can be commercially viable at scale.

Building the transportation network of the future

Accelerating zero-emission truck and bus infrastructure is a cornerstone of market transformation. It unlocks operational efficiencies, lowers total cost of ownership, and enables scalable deployment across regions. Achieving this requires optimizing charging locations, prioritizing known freight hubs, and integrating distributed and mobile energy solutions that reduce costs and meet near-term demand with flexibility.

Planning infrastructure in stages, rather than assuming an immediate transition, ensures growth aligns with real-world operational needs. Thoughtful, early-stage planning is essential. Freight is inherently precise: routes are optimized, schedules are tight, and margins are thin. Identifying freight hubs where shippers and logistics providers have established warehouses, ports, and depots provides a natural starting point for connecting the broader network. From there, blending public and private charging solutions can accelerate deployment and improve reliability.

This vision will only be realized through horizontal integration across the entire zero-emission transportation value chain—energy providers, technology OEMs, charge point operators, shippers, fleets, and others. Corridor planning efforts, such as the Global Green Road Corridors Initiative, exemplify this approach by concentrating investment along high-impact routes, convening key stakeholders, and driving collective commitment to shared standards and interoperability.

Catalyzing systems: Global Green Road Corridors

Road corridors are essential to trade and logistics, integrating supply chains, linking regions, driving economic growth, and delivering a range of benefits to the communities they connect. They connect ports to hubs to cities enabling a complete system to move goods, services and people. Green road corridors enhance traditional transport corridors embedding sustainability and resilience into their design and function. By supporting the deployment of zero-emission medium- and heavy-duty vehicles (ZE-MHDVs), they reduce environmental and health impacts while expanding the operational range of vehicles to tackle more demanding routes with greater efficiency. These corridors cut air pollution and greenhouse gases, support climate goals, and lower fuel costs. They also create future-proof jobs in transport, infrastructure, and renewable energy. Critically, by expanding public and semi-public infrastructure, green corridors ensure a just transition by giving small and medium enterprises access to charging and refueling facilities.

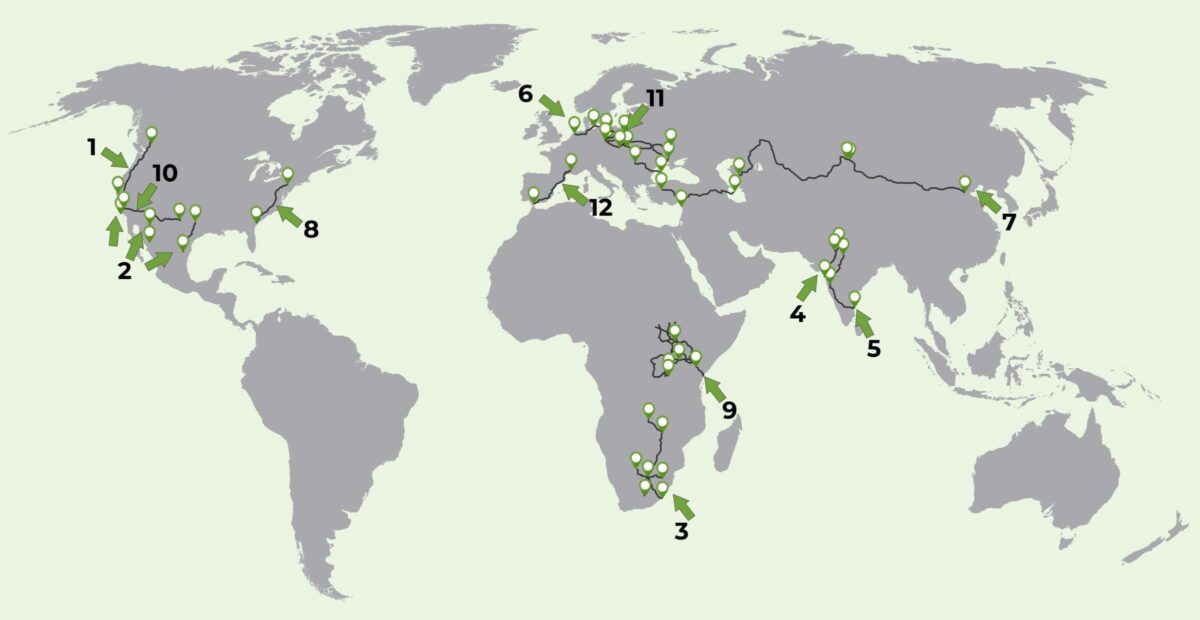

Corridors Supported by the Global Green Road Corridors Initiative

Corridor Legend: 1. FIFA 2026 Corridor (Canada–United States–Mexico). 2. United States–Mexico border corridors (California – Baja California, Texas – Nuevo Leon, Arizona – Sonora). 3. Southern Africa Container Corridor (Port of Durban, including South Africa, Lesotho, Eswatini, Zimbabwe, Botswana and Zambia). 4. India Corridor I (Mumbai–Delhi and Delhi–Jaipur). 5. India Corridor II (NH48: Delhi – Mumbai – Chennai). 6. European Corridor to Zero (the Netherlands, Germany, Poland and Ukraine). 7. Trans-Caspian International Transport Route (TITR) Corridor (China, through Kazakhstan, Azerbaijan, Georgia and Türkiye to Europe). 8. United States I–95 Corridor (Georgia – New Jersey).

The Global Green Road Corridors Initiative is an ambitious effort to advance a diverse set of the world’s road corridors to transition to a ZE-MHDV ecosystem. These autonomous corridors, each led and/or supported by an array of partners worldwide, will establish the basis for replicable, adaptable models that will serve as a real-time resource and framework for growth and success. The initiative is supported by a multilateral collaboration of 11 leading organizations including governments, nonprofits, financing institutions, and international development organizations as well as numerous partners on the ground, driving implementation forward across the world.

Over the last year the Global Green Road Corridors (GGRC) initiative expanded its scope by adding four new corridors to its portfolio of support: Africa’s Northern Corridor, the U.S. I-10 Corridor, the Germany–Poland Corridor, and the Mediterranean Corridor. This expansion enhances the initiative’s geographical diversity and strengthens its potential to foster global best practices. Below are the corridors visualized on a map, highlighting the cross-cutting geographies covered by this growing initiative.

As-a-service providers: Bridging the implementation gap

There is growing momentum to rethink business models that make ZE-MHDV deployment more cost-effective. Emerging “as-a-service” approaches shift upfront capital costs into predictable operating expenses. Charging-as-a-Service (CaaS) offers turnkey charging solutions; Infrastructure-as-a-Service (IaaS) adds renewables, storage, and resiliency; and Electrification-as-a-Service (EaaS) bundles vehicles, charging, and energy systems into one package—similar to leasing but designed for zero-emission fleets (see Figure below).

Types of “As-a-service” models

Already, several as-a-service providers are operating in markets around the world to facilitate faster adoption of supportive infrastructure, and in some cases, trucks as well.

From the Global MOU endorser community, Zeem Solutions provides a turnkey model that bundles vehicle leasing, charging, parking, maintenance, and energy services, allowing fleets to electrify without major capital investment. Zenobē combines financing, fleet electrification, and “battery-as-a-service,” pairing EV leasing with energy storage and grid integration to cut lifetime costs. In emerging markets, OX Delivers offers “truck-as-a-service,” designing rugged electric trucks and a digital logistics platform to support trade in challenging conditions. WattEV advances a similar approach in the U.S., operating electric trucks alongside public high-power charging depots, making freight electrification easier while scaling charging infrastructure. JUNA, a joint venture between Scania and Sennder, is pioneering “truck-as-a-service” in Europe, offering shippers access to zero-emission trucks through flexible contracts that bundle vehicles, charging, and digital logistics solutions, reducing risk for operators and accelerating adoption.

Faster fueling with megawatt charging systems

Refueling speed is one of the biggest hurdles for electric trucks. While diesel tanks fill in 5–10 minutes, today’s DC fast chargers take roughly an hour to add a few hundred miles of range. The new Megawatt Charging System (MCS) changes the equation, delivering up to 3.75 MW of power and cutting charging times to about 20 minutes. While almost no vehicles on the market today can accept that amount of power, there are more trucks becoming available that can receive close to 1 MW, significantly accelerating the time it takes to charge and up-time of the vehicle. Limited deployments of MCS have been rolled out in parts of Europe, led by Milence, a joint venture between Daimler, TRATON, and Volvo, and plans on developing over 284 MCS sites in Europe by 2027.

The emergence of MCS technology brightens the outlook for zero-emission freight by tackling two major hurdles: range and refueling time. Coupled with advances in battery efficiency, MCS can add hundreds of miles during a short stop, expanding operational range and keeping trucks on the road. As the network grows, trucks may rely on smaller batteries, reducing weight and boosting payloads while ensuring reliable opportunity charging.

Enabling Conditions for Destination 2040

Destination 2040: A global vision for zero emission transportation

To reach Destination 2040, emerging markets and developing economies have a powerful opportunity to leapfrog past diesel and build the foundation of a clean, resilient transport future. By sharing solutions and collaborating across sectors, all countries can accelerate progress toward a decarbonized global transport system—unlocking new industries, more efficient trade, and job growth in the green economy. By investing in zero-emission transport and logistics, nations can reduce their exposure to volatile global fuel markets, strengthen energy independence, and improve public health. This means building the infrastructure and workforce of the future: technicians, drivers, manufacturers, and innovators powering a modern, zero-emission economy.

As champions and changemakers from around the world unite under a shared ambition to eliminate commercial vehicle emissions, what once seemed impossible is now within reach. The shift to clean, zero-emission transportation is inevitable. While challenges remain, momentum continues to build, and history will remember those who drove progress forward—not those who stood in its way.

There is no single solution that fits every context on the path to Destination 2040. Yet around the world, countries and companies face many of the same challenges and opportunities, often shaped by regional circumstances. There is no need to reinvent the wheel—perhaps just electrify it. Proven solutions already exist that can drive large-scale adoption, including policies that create market certainty, financial mechanisms that reduce risk for fleets and investors, and coordinated approaches that ensure infrastructure is built efficiently to maximize utilization. Achieving these goals will require leadership and collaboration from both the public and private sectors, with companies and governments working together to accelerate zero-emission transport. The following recommendations outline the enabling conditions needed to accelerate progress and align global efforts for the benefit of people, the economy, and the planet.

Enabling conditions: Policy

Policy is the cornerstone of ZE-MHDV adoption, sending powerful market signals and providing the long-term certainty needed to mobilize private investment. The following recommendations aim to unlock policy-driven momentum across the commercial vehicle sector to transition the whole of the transport system.

Supply side regulations are made a top policy priority:

ZEV mandates are the simplest and cheapest regulation to set up, monitor, and enforce, locking in the pace of the transition and accelerating cost reductions through increased investments in innovation and production at scale. Fuel efficiency standards and CO2 regulations for tailpipe emissions offer alternative pathways to ensure automakers transition their vehicle technology to ZE.

Local and municipal leadership accelerates national progress:

Cities, states, and regions are uniquely positioned to drive innovation and demonstrate what’s possible. By piloting new policy approaches, building local coalitions, and fostering public–private partnerships, they can create replicable models that inform and strengthen national strategies. In contexts where national frameworks are emerging, local governments can act as powerful accelerators—translating ambition into action and showcasing tangible impacts that inspire broader adoption.

National carbon pricing schemes are introduced that account for MHDV emissions:

Carbon pricing, cap-and-trade, and emissions trading systems are different ways governments can impose limits on carbon emissions by industry to incentivize transitioning to clean alternatives. Companies will be rewarded for innovating, while laggards must pay to pollute if they surpass limits. These schemes must be carefully structured, or they can result in a paper exercise.

Diesel phase-out requirements introduced in importer markets:

While some nations produce their own vehicles, many others rely on imports—often resulting in an influx of older, less efficient vehicles, particularly in developing economies. Diesel phase-out regulations, or restrictions on imports, not only influence secondary markets but can also establish direct barriers that prohibit the entry of outdated, high-emission vehicles. Conversely, exporter countries can adopt complementary policies that restrict the export of such vehicles, preventing the displacement of pollution burdens onto emerging markets and supporting a truly equitable global transition away from diesel.

Enabling conditions: Infrastructure

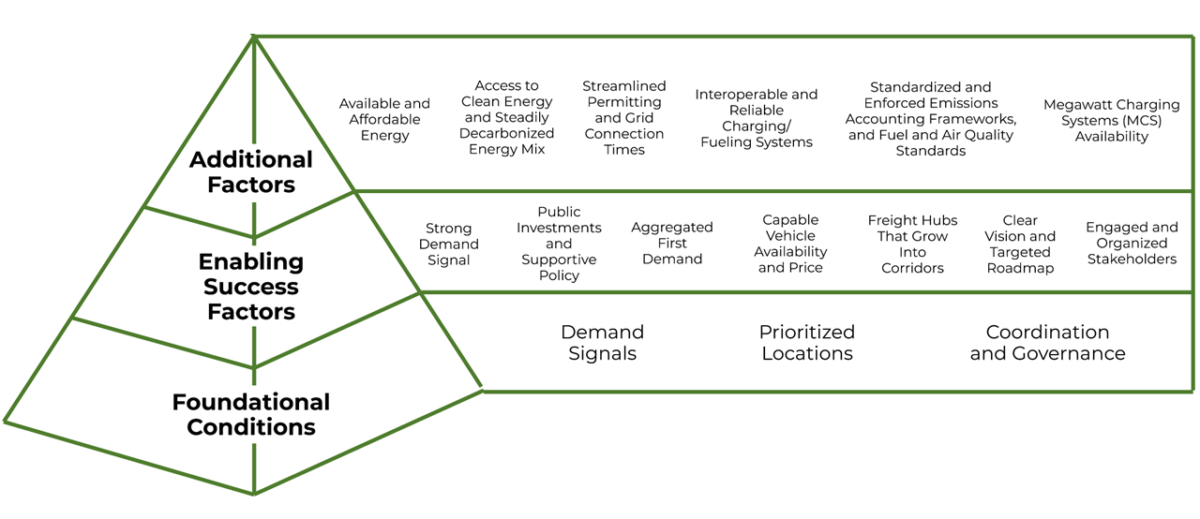

Building out the clean power and charging network of the future requires unprecedented collaboration across sectors. Beginning with ports and freight hubs as early targets for development, the network can be connected along key routes and highways to boost operational capabilities. Corridors, as the next phase, are essential for enabling longer trips without requiring oversized batteries, lowering costs while extending the range of ZE-MHDVs. Establishing this network requires close coordination across transportation and energy sectors, often spanning local and national borders. Governments, investors, grid operators, utilities, fleets, and communities must work together to deliver these complex, multi-year projects to achieve utilization and profitability. To meet the Global MOU’s 2030 milestones and achieve full transition by 2040, action must begin now. The figure below highlights the foundational aspects of establishing an ecosystem of enabling factors to allow corridor development to thrive.

Key Elements of a Successful Global Green Road Corridor Ecosystem

The following recommendations outline the steps needed to drive progress.

Governments

Set clear direction and provide certainty: Establish ambitious goals, strong regulations, and equitable policies to accelerate ZE-MHDV adoption in alignment with the 2030 and 2040 targets of the Global MOU. Develop phased national and sub-national freight infrastructure plans to identify priority hubs and corridors, and co-fund projects that reduce vehicle costs and expand infrastructure access.

Mobilize collaboration and investment: Coordinate stakeholders across levels of government, utilities, and the private sector to speed corridor development, ensure grid readiness, and support renewable energy integration. Promote innovative financial mechanisms and inclusive access to them, while engaging global partnerships like the Global Green Road Corridors initiative to scale solutions.

Transport sector

Lead through pilots and partnerships: Prioritize decarbonization by integrating ZE-MHDVs into operations, launching pilot projects along corridors, and collecting data to inform future investment and scaling decisions.

Build the case through collaboration: Work with shippers, carriers, utilities, and governments to aggregate procurement, share infrastructure, and develop financing models that demonstrate both the economic and operational value of zero-emission freight, strengthening the business case for broader adoption.

Energy/power sector

Plan and build for ZE-MHDV integration: Prioritize the needs of zero-emission transportation in all grid modernization efforts, collaborating with governments and industry to strengthen hub and corridor infrastructure, deploy charging and hydrogen refueling stations at strategic freight locations, and expand distribution grid capacity to support rapid, large-scale connections.

Deliver clean, affordable, and reliable power: Invest in renewable and decentralized energy systems to minimize emissions, while offering competitive pricing and innovative business models that mitigate high demand charges. Use long-term power purchase agreements and other financial tools to ensure stable energy supply and predictable costs for ZE-MHDV operators.

Enabling conditions: Finance

Breaking down prohibitive costs is paramount to broadening the business case for ZE-MHDVs. While generally more expensive up-front today, ZE-MHDVs enable significant cost savings for fleets and business over their lifetime. On the road to 2040, key measures can be implemented to bring forward the cost parity and ensure public capital is leveraged to unlock private sector investments to build the economies of scale needed to put downward pressure on cost in markets around the world. The following steps should be advanced to enable greater access to ZE-MHDVs, particularly where they are needed the most.

Create long-term certainty that facilitates investments and economies of scale:

Supply-side regulations create the market certainty needed for manufacturers to ramp up production and bring down per-unit prices. They are shown to be more effective than carbon pricing and incentives to sustainably reduce prices over the long term. Additionally, they can encourage manufacturers to offer discounts on ZEVs in order to meet regulatory targets and avoid fines.

Address the most influential factors getting in the way of TCO parity:

The cost structure for zero-emission trucks varies substantially by country. In most cases, electricity pricing will have the largest impact on TCO. Other key factors can be diesel prices, import tariffs, road tolls, grid infrastructure expansion, and residual values. Targeted interventions can help overcome many of these constraints, either by reducing punitively high costs for ZE-MHDVs, or by internalizing costs for ICEVs that are usually passed on to communities and health systems. Time-of-use electricity tariffs, removing diesel subsidies, preferential road tolls, proactive grid investments, and residual value guarantees are some of the tools available to policymakers to do so, the relevance of which will vary by context.

Develop programs to mitigate risks for fleets and carriers to bridge financing gaps and reduce uncertainty:

Implementing targeted programs such as residual value guarantees are a capital-efficient way to reduce costs for businesses and governments, and maximize private sector investment all while giving peace-of-mind to fleets and investors wanting to scale. Similarly, credit-risk guarantees can help democratize access to ZE-MHDVs, contributing to a just transition that engages SMEs in the process and helps prepare financiers to better support the largest segment of truck owners and operators to date.

Charging Ahead Together

Ready to reach Destination 2040?

Drive to Zero can help. With the backing of 42 national governments and more than 270 private sector innovators and businesses, the Global MOU is the flagship effort driving zero-emission commercial vehicle decarbonization worldwide. Join us.

Sign or endorse the Global MOU!

A first step on this journey is to set your ambition for what is possible. By signing the Global MOU as a national government you work collaboratively with other national governments working to reach 100% new sales of zero-emission medium- and heavy-duty vehicles by 2040. As an endorser, you commit to actions for your fleet, manufacturing, financing or other interests to help achieve Global MOU goals. There are no prerequisites for signing or endorsing, or any need to have begun any of the interventions mentioned in this report. What matters is your readiness to commit and act. We are here to meet you where you are and turn ambition into action.

If there were areas of curiosity or inquiry with regard to this report, please reach out to info@globaldrivetozero.org. We are eager to field questions or dig deeper into the “how-to” aspects of the three pillars of Policy, Infrastructure Development, and Financing. Further, if a connection can be facilitated to any of the organizations mentioned above, please reach out.