The global zero-emission medium- and heavy-duty vehicle (ZE-MHDV) market has moved beyond pilots and prototypes. Today, it is defined by scale, diversity, and measurable performance gains. The data is unequivocal: momentum is accelerating across vehicle types, regions, and real-world applications.

As we enter 2026, we take a fresh look at the Zero-Emission Technology Inventory (ZETI), the leading global resource tracking zero-emission commercial vehicle availability and specifications. Since 2020, our team has continuously expanded ZETI’s capabilities by adding new features, broadening regional coverage, offering the platform in multiple languages, and keeping pace with a rapidly evolving market.

That evolution is being driven by a global push to decarbonize commercial transport. Even as governments debate efficiency standards and deploy incentive programs, manufacturers worldwide are racing to lower costs, extend range, improve reliability, and deliver vehicles capable of meeting demanding commercial operations. Reflecting this shift, ZETI has grown well beyond its early focus on the United States and Europe. Today, it tracks zero-emission commercial vehicles across more than 12 countries, spanning every continent except Antarctica, for now…

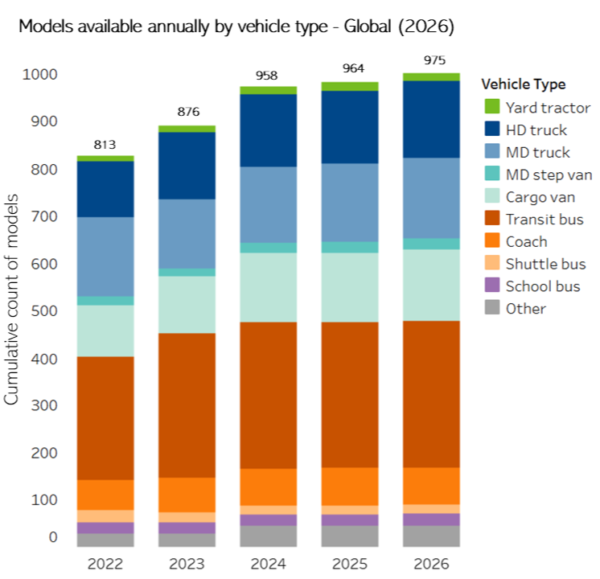

Models available annually by vehicle type – global (2026)

ZETI data shows steady growth in model availability across all vehicle segments over the past several years, underscoring the need for OEMs to innovate and diversify their offerings in response to rapid advances in vehicle electrification worldwide. In 2022, approximately 813 ZE-MHDV models were available globally, produced by 156 OEMs. By 2025, that number had increased to 964 models from 170 OEMs. The figure on the right illustrates this growth and the distribution across vehicle types.

Zero-emission buses continue to dominate the market. In 2025, full-sized transit buses accounted for 310 available models, compared with 164 medium-duty trucks, 154 heavy-duty trucks, and 145 cargo vans. While overall availability has increased, the pace of growth has shifted over time. The sharpest expansion occurred through 2021, followed by a noticeable leveling off beginning in 2022.

This pattern reflects broader market dynamics. As advanced regulatory frameworks took hold in regions such as Europe and the United States, targeting improved vehicle efficiency and reduced CO₂ emissions, OEMs were compelled to move beyond internal combustion platforms. That pressure drove a rapid increase in zero-emission model introductions during the market’s early growth phase.

More recently, the slowing rate of new model introductions suggests the market is entering a more mature phase. Rather than launching entirely new platforms, OEMs are increasingly refining and upgrading vehicles with established demand. This shift is visible across the industry, from iterative improvements to models such as the Freightliner eCascadia and DAF CF to continued development of proven platforms like BYD’s 8T.

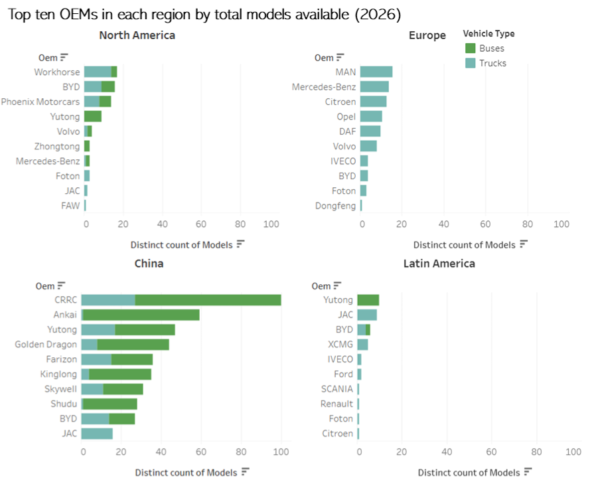

Top ten OEMs in each region by total models available (2026)

As the market matures, it is also consolidating. Many start-ups and smaller pure zero-emission entrants have struggled amid challenging market conditions and rising barriers to entry, particularly when competing with long-established manufacturers offering proven reliability and customer trust. Several high-profile companies, including Lion Electric, Volta, Nikola, and Lightning eMotors, have faced bankruptcy or restructuring, often resulting in asset acquisitions by more established players.

At the same time, regional policy environments continue to shape where new products succeed. In the United States, the number of OEMs offering zero-emission heavy-duty trucks has declined by approximately 11 percent from 2022 to 2026. In contrast, China has experienced nearly a 47 percent increase over the same time period. As federal incentives in the U.S. have been scaled back and state-level policy momentum has weakened, other regions have continued to advance through stronger regulatory signals and sustained market support.

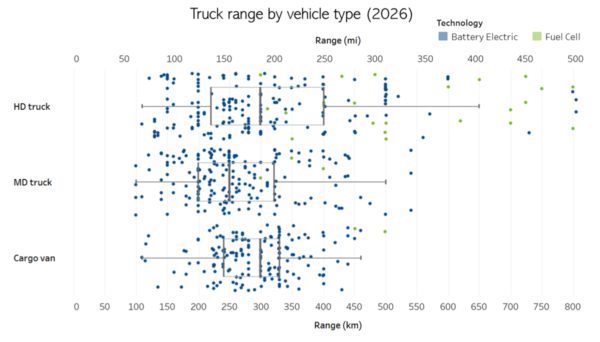

Despite these regional differences, the long-term outlook remains positive. Competition among remaining OEMs is intensifying, driving cost down and motivating advances in range, charging speed, durability, and towing capability. Range data in particular reveals a critical insight: technology is no longer the limiting factor for many commercial applications.

Truck range by vehicle type

The figure below illustrates manufacturer-reported range capabilities for zero-emission truck models across heavy-duty trucks, medium-duty trucks, and cargo vans. The median range for zero-emission heavy-duty trucks is approximately 186 miles (300 kilometers), with top-end models approaching 500 miles (800 kilometers). These capabilities comfortably support most local and regional haul duty cycles. For example, trucks operating in port drayage often travel roughly 140 miles per day, well within the performance envelope of today’s zero-emission heavy-duty platforms. Zero-emission cargo vans show similar average range performance, while medium-duty trucks typically offer slightly lower range but operate on shorter routes. Across all three segments, the majority of daily commercial operations fall squarely within existing vehicle capabilities.

Taken together, these trends point to a market that is transitioning from early expansion to durable scale. The technical foundation for widespread adoption of zero-emission commercial vehicles is firmly in place. The challenges ahead are increasingly practical and systemic, centered on affordability, infrastructure, and policy alignment. Addressing these factors will determine how quickly today’s technological readiness translates into broad, real-world deployment.

As 42 countries representing roughly one-in-four trucks globally move toward an ambitious goal of 100% new zero-emission truck and bus sales by 2040, strong investments in infrastructure like green corridors, financial tools, and ambitious policies will help ensure ZE-MHDV market growth and maturation.