India’s freight system sits at the center of its economic engine—and its energy vulnerability. Nearly 12 million diesel trucks move ~70% of the country’s freight, consuming 55% of national diesel demand and driving an estimated USD 50 billion annual fuel spend. This dependence is increasingly costly: with a crude import bill of USD 137 billion (FY 2024–25), every USD 10/bbl increase adds USD 14–16 billion to India’s import burden. Freight, therefore, is not just a transport issue—it is a macroeconomic risk. This is exactly why the shift to Zero-Emission Trucks (ZETs) is no longer optional but inevitable— and not just for the sake of decarbonisation, but for energy and economic security, cost stability, and supply chain resilience.

A Decade of Diverging Energy Economics

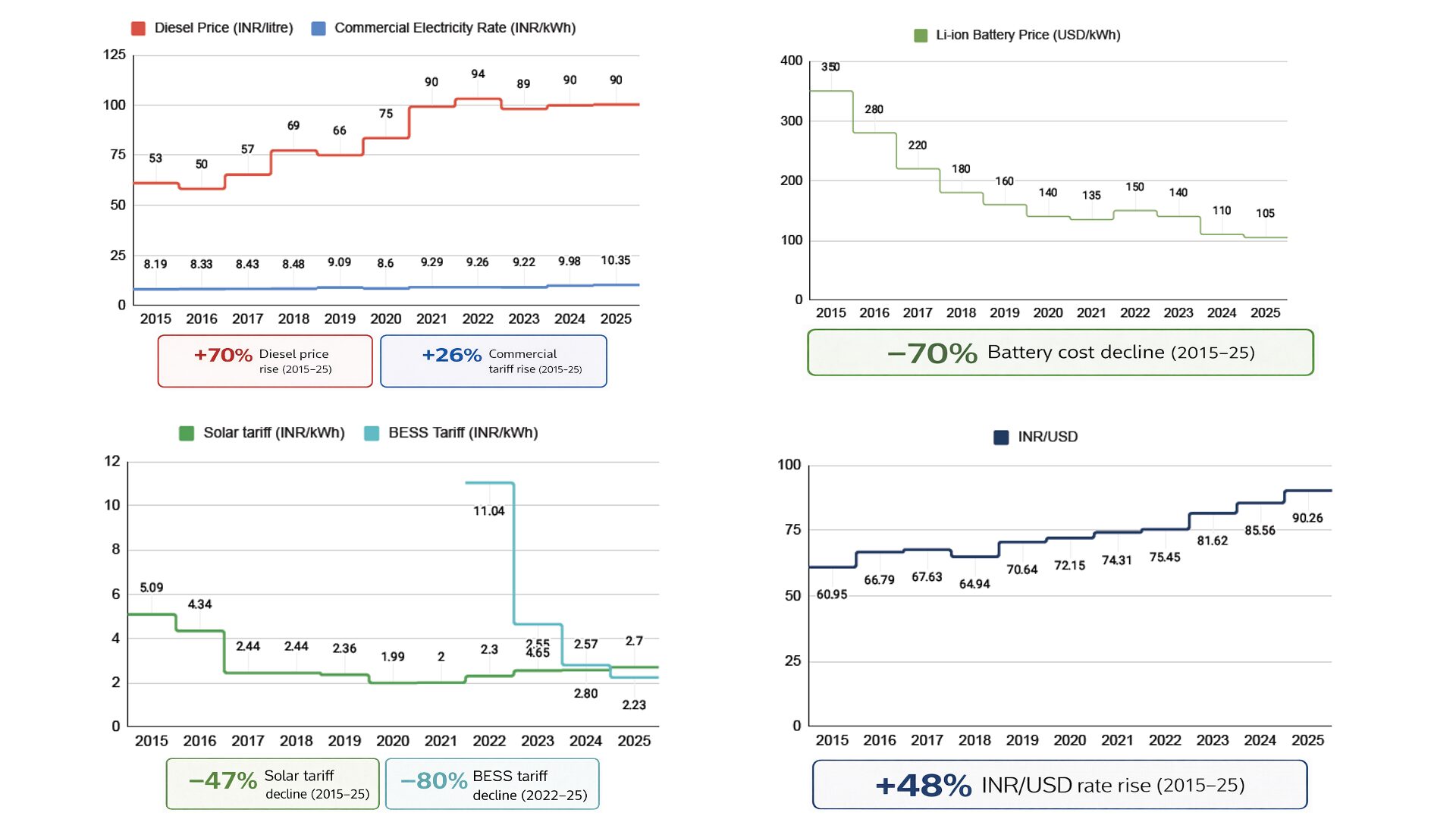

Over the past decade, the cost trajectories of diesel and clean energy have fundamentally diverged:

- Diesel prices: INR 53/L → INR 90/L (increased 69%)

- Commercial electricity tariffs: INR 8.19/kWh → INR 10.35/kWh ( increased 26%)

- Solar tariffs: INR 5.09/kWh → INR 2.7/kWh (reduced 47%)

- Global li-ion batteries prices: USD 350/kWh → ~USD 105/kWh (reduced 70%)

- Battery Energy Storage System (BESS) tariffs in India: INR 10.83→INR 2.08/kWh (reduced 80%)

- INR against USD: INR 60.95→INR 90.26 (depreciated 48%)

- Goods and Service Tax (GST) on diesel trucks is 13% higher than ZETs

Fig.1 India’s Energy Cost Transition: Rising Diesel Prices vs Declining Battery Costs (2015–2025)

Source: CALSTART/Drive to Zero India Analysis, 2026

These trends tell a clear story: Diesel is becoming structurally more expensive and volatile, while electricity—especially renewable-backed—is becoming cheaper, more predictable, and domestically anchored. RE+BESS (renewable energy + battery energy storage systems) is the new competitive energy baseline.

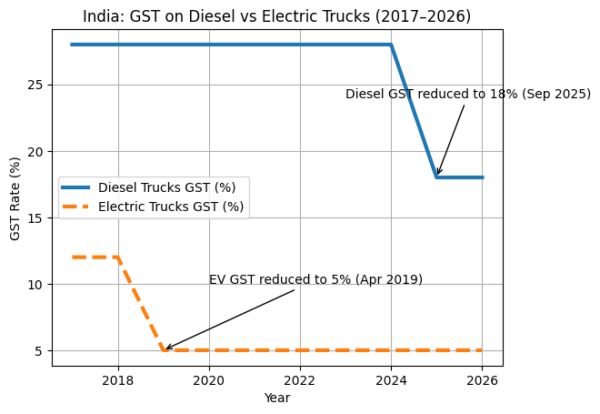

Even where electricity tariffs have risen modestly, they remain insulated from global shocks and increasingly benefit from falling renewable costs. This divergence is now reinforced by fiscal policy—electric trucks attract just 5% GST, while diesel trucks face significantly higher tax (18%) burdens.

Fig.2 India: GST on Diesel vs Electric Trucks (2017–2026)

Source: CALSTART/Drive to Zero India Analysis, 2026

Early Signals of Market Shift

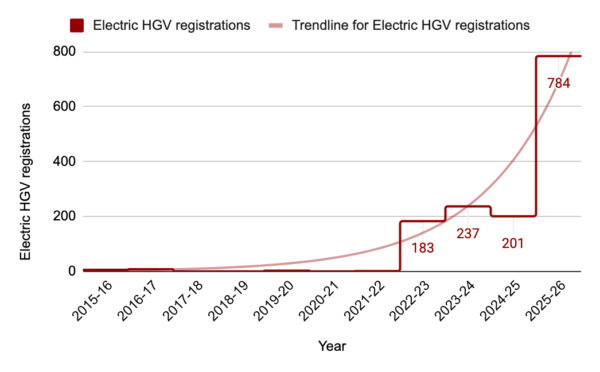

India has already established a strong foundation for its zero-emission medium- and heavy-duty segment (ZE-MHDVs), registering 4,441 electric buses in 2025. After establishing this critical technology foundation for ZE-MHDVs, India’s heavy-duty electric truck segment is now entering a breakout phase. Registrations increased from 201 (2024–25) to 784 (2025–26)—a nearly 290% year-on-year growth. Adoption is concentrated in closed-loop applications such as cement, mining, Fast-Moving Consumer Goods (FMCG), and ports, where high asset utilization supports viable business models. At the same time, technology readiness is no longer a constraint. Over 25+ medium- and heavy-duty electric truck models are now available in India, with proven performance in real-world conditions.

Fig.3 India: Electric Heavy Goods Vehicle Registrations (2015–2025)

Source: NITI Aayog (https://iced.niti.gov.in/analytics/ice-and-ev-vehicle-registered) & CALSTART/Drive to Zero India Analysis, 2026

Fig.4 CALSTART (2026): CALSTART/Drive to Zero’s Zero-Emission Technology Inventory (ZETI). Available online at: https://globaldrivetozero.org/tools/zeti/

Click here to access 1,000+ ZE-MHDT global model data available from CALSTART Drive to Zero’s Zero Emission Technology Inventory (ZETI).

From Cost Parity to Cost Advantage

The implications for freight economics are profound. As battery costs continue to decline and utilization improves, ZETs are moving beyond parity into sustained cost advantage. On high-utilization corridors (>10,000 km/month), electric trucks can already achieve ~24% lower total cost of ownership than diesel alternatives. This is not a future scenario—it is already visible in the market.

India is Charging up Change

Watch to learn how India is charging up for change. In this video from CALSTART’s Drive to Zero, we’re introduced to UltraTech, the country’s largest cement producer, which has recently begun electrifying its fleet. We also hear from NITI Aayog, a policy think-tank of the Government of India, which believes regulations and partnership will accelerate the shift to electric vehicles.

Fig.5 India: HDV e-truck transporting clinker to grinding unit

Industry Momentum: From Commitment to Deployment

This transition is now being actively accelerated by India’s leading industry players under the Global MoU for Zero-Emission MHDVs, translating ambition into on-ground deployment and investment. Companies such as EKA Mobility, Montra Electric (formerly IPL Tech), Blue Energy Motors, and Transvolt Mobility, BillionE, Switchlabs, Greencell Mobility, INTENT, are scaling manufacturing and deployment—ranging from multi-million investments in electric truck production to large-scale ZE-MHDV deployments including battery-swappable heavy vehicles. At the same time, ecosystem players like ChargeZone are building high-capacity corridor charging networks, while Sun Mobility is advancing certified battery-swapping solutions for heavy-duty applications. Together, these commitments signal a coordinated industry shift—where OEMs, operators, and infrastructure providers are aligning with global targets to accelerate e-truck adoption in India.

Sub-National Leadership: From Policy to Implementation

Global MoU endorsers Telangana and Goa are translating ambition into implementation. Telangana is driving EV manufacturing, incentives, and charging infrastructure for trucks and buses, while Goa is advancing public transport electrification and integrated charging ecosystems. Together, they are de-risking early markets and crowding in private investment. These states offer replicable models for scaling zero-emission freight across India.

Click here to join the Global MoU network.

The Policy Window: From Pilots to Systemic Scale

India has already laid the fiscal and regulatory foundation for this transition. What is needed now is clear market signaling through regulations and coordinated execution at scale:

- Set explicit ZE-MHDV soft targets aligned with the Global MoU trajectory

- Embed freight electrification within India’s Harmonised Infrastructure List (HIL) and National Determined Contributions (NDCs)

- Finalize Corporate Average Fuel Economy (CAFÉ-3) standards and emission standards (Bharat Stage VII) regulations for MHDVs to drive supply-side transformation

- Financing models aligned with high-capex, long-tenor assets and de-risking products enhancing cash flow certainty for Financial Institutions (FIs).

These actions will move the sector from early pilots to system-wide adoption, unlocking investment, infrastructure buildout, and industry alignment.

Click here to explore the enabling conditions for Destination 2040: A global vision for zero emission transportation and journey of 40+ Global MoU signatory countries.

A Structural Shift Underway

India’s freight sector is at a decisive turning point. The economics are shifting, the technology is ready, and early adoption signals are strong. What remains is translating this momentum into scale. The transition to zero-emission trucks is increasingly an economic decision grounded in energy security, cost stability, and industrial competitiveness.

The question is no longer if India will electrify freight—but how fast it can do so to reap the benefits of the energy resilience to its economy.